Owning a home is a big dream for many. It comes with a lot of joy and many new things to learn. One of the most important is your escrow account. If you’ve ever looked at your mortgage statement, you may have seen the line “what is escrow balance.” This can be confusing. But in this guide, we will walk you through exactly what that number means. We will explain why it matters to you as a homeowner.

What is Escrow Balance?

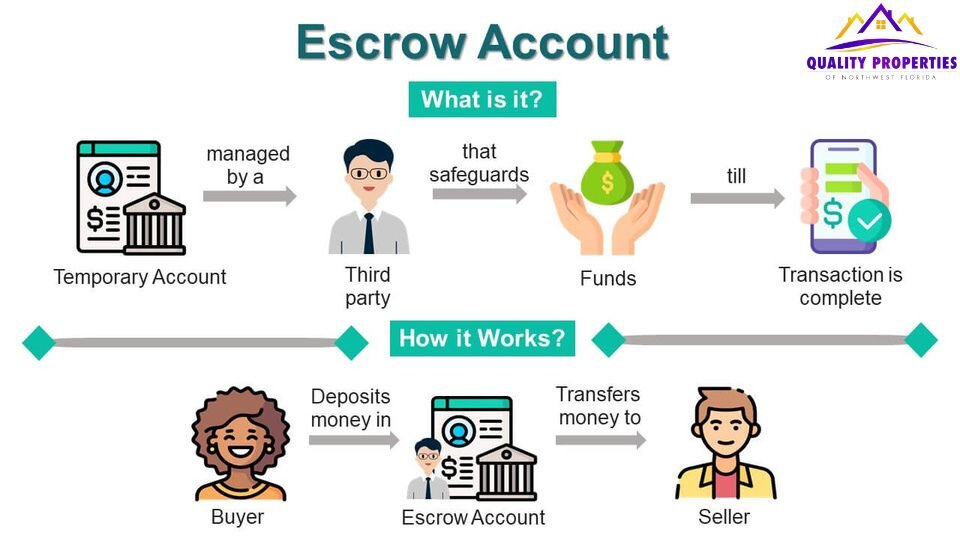

An escrow balance is just a savings account for your home’s big bills. It is managed by your mortgage company. This account pays for things like property taxes and homeowner’s insurance. These are often called your PITI payments. The I and the T stand for insurance and taxes. The P and I are for principal and interest. Your mortgage lender sets up this account. They do it to make sure those big bills are paid on time. This protects them and you.

Understanding Escrow Accounts in Your Home Loan

When you get a home loan, you make a monthly payment. This payment is usually for two things. The first part goes to your loan itself. This is the principal and interest. The second part goes into your escrow account, and this money builds up over the year. It’s used to pay your large bills when they are due. This is the escrow balance meaning. It’s the total money saved up in that account right now. Did you know that? This system helps you avoid one massive bill. Instead, you pay a small amount each month.

Why Lenders Require Escrow Accounts

Lenders want to protect their investment. The home is the collateral for the loan. If property taxes go unpaid, the government can put a lien on the house. Whether the homeowner’s insurance lapses, the house is not protected. The lender could lose their money. Requiring an escrow account makes sure these bills are always paid. This protects everyone. It gives the homeowner peace of mind. They know those crucial bills are handled.

How Escrow Accounts Work for Homeowners

Every month, a piece of your mortgage payment goes into the escrow account. The amount is calculated based on your yearly property taxes and insurance premiums. Your lender divides these yearly costs by 12. They add that amount to your monthly mortgage payment. This is why your full payment is often more than just the principal and interest. The money sits in the account. It waits until the bills are due. When a tax bill or an insurance premium is due, the lender pays it from your account. Your escrow balance then goes down. It’s a quite simple and efficient system.

The Mortgage Escrow Analysis

Every year, your mortgage company does a review. They look at your escrow account and check what you paid in versus what was paid out. This review is called a mortgage escrow analysis. They do this to see if the amount they are collecting is right and check if your property taxes or insurance premiums went up or down.

Escrow Shortage vs Surplus

Sometimes, the analysis shows a problem. If the bills were higher than what was collected, you have an escrow shortage balance. This is also known as a negative escrow balance. It means there is not enough money in your account. The lender may require a lump sum payment from you. They may also increase your monthly payment to make up for the shortage and want to avoid what if escrow balance is negative problem in the future.

On the other hand, a good thing can happen too. If your bills were less than what was collected, you have a surplus. The lender will often send you an escrow refund. This is a pleasant surprise. They might also lower your monthly payment to correct the balance. Knowing the difference between an escrow shortage vs surplus is key. It helps you understand your mortgage statement better.

This is a suitable time to remember something. Managing your finances can be simple with the right help. If you ever need to sell your house fast, for any reason, Quality Properties of Northwest Florida LLC can make a fair cash offer.

Escrow Cushion Requirements

Lenders are smart about these things. They don’t want to deal with a negative escrow balance either. So, they can keep a small cushion in your account. This is usually up to one-sixth of your total yearly bills. It’s to protect against small increases in taxes or insurance. This is what escrow cushion requirements are all about.

How to Check Your Escrow Balance

You can find out your escrow balance in a few simple ways. The easiest way is to look at your monthly mortgage statement and this statement will show your full payment. It will also break down where your money goes. You will see lines for principal, interest, and the money that went into your escrow account. The statement will also show the current escrow balance on mortgage statement. This is the clearest picture of where you stand.

You can also call your mortgage company. Just ask them for your current escrow balance. They can also give you details about the last analysis. Most mortgage companies also have an online portal. You can log in and see your account details in real time. This is the best way if you are worried about how to check escrow balance.

Why is My Escrow Balance so High?

People get worried when they see a substantial number in their escrow balance. A high balance is not always a dreadful thing. It usually means one of two things. First, you may have just made a payment. The money hasn’t been used yet. So, the balance is high. Second, it could be a sign of a coming bill. For example, your property taxes are due in two months. Your balance will be growing to prepare for that large payment. A high escrow balance is good. It means you are ready for the bills.

What Happens If Escrow Balance Is Low?

A low escrow balance is the bigger concern. It means you might not have enough money to pay the next big bill. This could be your property taxes or home insurance. If this happens, your mortgage company will notice during the yearly analysis. They will notify you. You will need to make up the difference. This can be a one-time payment. Or they will raise your monthly payment for the next year. This is what happens if the escrow balance is low.

Escrow Balance and Home Insurance Payments

Your escrow account pays your home insurance premium. Insurance costs change all the time. They can go up due to storms or other claims in your area. This increase directly impacts your escrow balance and home insurance payments. If your premium goes up, your monthly escrow payment will also likely go up. The lender needs to collect enough money to pay the new higher bill. It is important to know your premium amount. You can compare it to your escrow balance statement explained document to make sure it matches.

Who Manages Escrow Account Balance?

The mortgage servicer manages your escrow account balance. This is the company you send your monthly payment to. They are responsible for making sure the bills are paid on time and receiving your money each month. Servicer hold it in the account. When the tax or insurance bills come, they pay them. Mortgage servicer also sends you an annual escrow balance statement explained in the letter. This letter shows you all the money that came in and went out.

Escrow Balance and Property Taxes

Property taxes are a big part of your escrow account. Tax rates can change. They can go up or down. If your local government raises property taxes, your escrow payment will also increase. This is because the lender needs to collect more money to cover the higher tax bill. In fact, this is the link between your escrow balance and property taxes. Keeping an eye on your local tax rates can help you understand why your monthly payment might change.

Escrow Account vs Mortgage Payment

It’s easy to get these two. Your mortgage payment is the total amount you pay each month. This includes the principal, interest, and your escrow payment. The escrow account vs mortgage payment is a simple difference. One is the part. The other is the whole. A change in your escrow account will change your total mortgage payment. But your mortgage payment will not change the money in your escrow. The two are closely linked but are not the same thing.

Escrow Balance vs Escrow Shortage

Your escrow balance is the total money in the account at a given time. An escrow shortage is when that balance is too low to cover your upcoming bills. You can have a high escrow balance but still have a shortage if a huge property tax bill is coming due. The shortage is a problem. The balance is just a number.

Where Does Escrow Balance Go?

The money in your escrow account goes to a special bank account. This account is managed by your mortgage lender. They hold onto your money. They cannot use it for anything else. The money is used only to pay your property taxes and homeowner’s insurance. This is a secure system. Your money is protected. It’s an important part of a home loan.

Escrow Balance and Interest Rates

Many people ask about this. Do higher interest rates affect my escrow balance? The simple answer is no. The interest rate on your mortgage does not directly change the money in your escrow. Interest rate affects your principal and interest payment. Your escrow balance and interest rates are separate. However, the total monthly payment changes. But the escrow portion is based on taxes and insurance.

Final Words

For many homeowners, the escrow balance in mortgage is a safety net. It protects them from large, sudden bills, and helps with budgeting. It ensures that two of the most important bills, taxes and insurance, are always paid on time. This is why the escrow balance for homeowners is so important. Because it provides peace of mind and simplifies a complex part of homeownership.

If you are a homeowner and need to sell your house quickly without the hassle of a traditional sale, Quality Properties of Northwest Florida LLC can help.

FAQs

What is an escrow account and who needs one?

An escrow account is a special savings account. It is set up and managed by your mortgage lender and used to pay for your property taxes and homeowner’s insurance. Most people who get a mortgage need one. It is a requirement for many home loans.

What is the difference between an escrow balance and a closing balance?

The escrow balance vs closing balance are quite different. Escrow balance is the money in your account after you move in. It is for your ongoing bills. The closing balance is the total amount you paid on the day you closed in the house. It is funded with some of the money from your closing balance.

What happens to my escrow account when I sell my house?

When you sell your house, the account is closed. Your mortgage lender will do a final check. They will pay any remaining bills and send you a refund for any extra money left over in the account. This is the escrow balance refund after selling house.

Can I manage my own escrow account?

In some cases, yes. If you have enough equity in your home, you may be able to cancel the escrow account. You would then be responsible for paying your property taxes and homeowner’s insurance yourself. This is an option for some.

What if I have a negative escrow balance?

If you have a what if escrow balance is negative problem, your lender will let you know. They will offer you a choice. You can pay a lump sum to fix it. Or they will raise your monthly payment for the next year. The choice is yours. They need to collect enough money to cover your bills.

Is it good to have a high escrow balance?

Yes, in general. A high escrow balance means you have enough money. It means you are ready to pay your next big bill. It means your account is healthy.

{kind=link}